Finishing a driver’s education course is one of the smartest ways to get a real break on your car insurance. Most providers offer an insurance discount for drivers ed that can slice anywhere from 5% to 20% off your bill. Why the discount? Insurance companies see drivers who have completed a formal course as a much safer bet. Consequently, they reward that extra training with lower premiums.

How a Driver’s Education Course Puts Money Back in Your Pocket

Insurance is all about risk. When your provider calculates your premium, they are estimating how likely you are to be involved in a traffic incident. In their eyes, a driver with a certificate from a state-approved course is not just another person on the road. Instead, they are someone who has proven they understand the rules and take safety seriously. That simple piece of paper from your course changes their entire calculation. For instance, it signals that you are a lower risk, and that translates directly into savings for you. This is a huge advantage, especially for young drivers who usually get hit with the highest insurance rates right out of the gate.

What That Discount Actually Looks Like

Even a small percentage can make a big difference over a year. Let’s look at some numbers to see how a typical discount works on a standard policy. The savings often pay for the entire course within the first year alone, making it a fantastic investment.

Estimated Annual Savings with a Driver’s Ed Discount

This table shows what you might save annually on your car insurance premium by applying a common driver’s ed discount.

Annual Premium Before Discount

Potential Discount (15%)

Estimated Annual Savings

New Annual Premium

$2,000

$300

$300

$1,700

$3,000

$450

$450

$2,550

$4,500

$675

$675

$3,825

A Strategy Backed by Data

This is not just a friendly perk; it is a solid business decision for insurance companies. Their data consistently shows that formally educated drivers are involved in fewer collisions. Therefore, they file fewer claims. According to the National Highway Traffic Safety Administration (NHTSA), ongoing education is a key part of reducing roadway risks. It all boils down to this: taking a driver education course shows you are proactive about safety. As a result, that makes you a lower-risk customer and earns you a better rate. This benefit is not just for teens—even experienced drivers can take a defensive driving class to sharpen their skills and keep their premiums down.

Why New Drivers Face Higher Premiums

Ever get that sticker shock when you see an insurance quote for a new, young driver? It is a common experience, and it can feel a little unfair. However, it is not personal—it is all about risk, and insurance companies run on numbers. The hard truth is that statistics tell a consistent story. Simply put, inexperience behind the wheel translates to a higher chance of being in a traffic incident. This statistical reality is the single biggest reason why drivers under 25 often face the highest insurance premiums on the market. The Insurance Institute for Highway Safety (IIHS) provides extensive data showing that teen drivers have crash rates nearly 4 times those of drivers 20 and over per mile driven.

It All Comes Down to the Data

From an insurer’s perspective, every new driver is a blank slate. Without a long, spotless driving history to look at, they have to use general data trends. Unfortunately, those trends show that younger drivers, as a group, are involved in far more collisions than their more experienced counterparts. This is not a judgment on any one person’s ability. It is a risk calculation based on millions of data points gathered over decades. Because of this high-risk profile, it is not uncommon for young drivers to be quoted thousands of dollars a year for car insurance.

How Driver’s Ed Flips the Script

This is where earning an insurance discount for drivers ed becomes a game-changer. When a new driver completes a state-approved course, it gives the insurance company a solid, tangible reason to treat them differently. You are no longer just part of a high-risk demographic. Instead, you are now a driver who is formally trained and proactive about safety.

Completing a certified course is hard evidence that a new driver has learned critical defensive driving skills, hazard perception, and the rules of the road from professionals. It is a direct signal to insurers that you are a lower risk than your peers who have not taken a course.

That certificate proves a real commitment to being a responsible driver. You have gone from being just another statistic to an individual who has invested time and effort into being safer. That is exactly what insurers want to see, and they are happy to reward it with a meaningful discount.

Building Skills That Matter

So, what exactly do you learn in a driver’s ed course that makes such a big difference? It is all about building a solid foundation of skills that might otherwise take years of trial-and-error to develop. The curriculum is designed to target the biggest risk factors for new drivers:

Defensive Driving Techniques: This is the core of it all—learning to anticipate what other drivers might do and spotting potential dangers before they turn into real emergencies.

Collision Avoidance: You will practice specific maneuvers for dealing with sudden, unexpected situations, like a car pulling out in front of you.

Deep Understanding of Road Laws: This goes way beyond just memorizing facts to pass the permit test. You will learn the why behind the rules.

Building Real Confidence: The course gives you the tools to handle tricky situations like heavy freeway traffic or bad weather, helping you react with skill instead of panic.

By tackling these critical skill gaps head-on, a good driver’s ed program gives you the kind of training that statistics prove helps prevent collisions. That is why insurers are willing to offer a discount. For them, it is a smart bet on a safer driver. For you, it is an even smarter investment.

Finding a Course That Qualifies for a Discount

Securing an insurance discount for drivers ed is not as simple as signing up for the first course you find online. You have to be strategic. The reality is that many programs will not meet your insurance provider’s specific standards. Therefore, picking the right one from the start is crucial. The first thing to look for is state approval. This is the absolute baseline. In California, the Department of Motor Vehicles (DMV) sets the standards for what makes a legitimate driver education course. You can check your state’s official DMV or DOT website for a list of approved programs.

Always Check with Your Insurer First

Here is the single best piece of advice: call your insurance agent before you sign up for anything. This five-minute phone call can save you headaches and wasted money. Insurance companies keep their own lists of approved driver’s ed providers they know and trust. By calling, you get the information you need directly from the source. When you get your agent on the phone, ask these specific questions:

“Do you offer a discount for completing a driver’s education course?”

“Can you send me a list of your pre-approved schools or programs?”

“Are there any specific requirements, like a minimum number of in-car driving hours?”

“Do you accept online-only courses for the discount?”

This conversation takes all the guesswork out of the process. Your agent will lay out a clear path to earning that discount, ensuring the course you choose will actually result in savings.

What to Look for in a Qualifying Program

Once you have the green light from your insurer, you can start comparing your options. A high-quality, legitimate program will always have its credentials front and center. Here is what you should be on the lookout for:

Official State Approval: A reputable school will proudly display its state certification number on its website. If you cannot find it easily, that is a red flag.

Clear Curriculum Outline: The course description should tell you exactly what you will be learning, from state traffic laws and defensive driving tactics to hazard perception.

Defined Hour Requirements: The program must meet your state’s minimums for both classroom instruction and practical, behind-the-wheel training.

The goal is twofold: find a program that makes you a safer driver while also ticking all the boxes your insurance company requires. A state-approved course is the key to accomplishing both.

State Spotlight: California’s “Move Over” Law

Every state has specific roadway laws that drivers must know. In California, the “Move Over” law is a critical one for safety. According to the California Department of Motor Vehicles, this law requires drivers to move over a lane or, if unable to do so, slow down when approaching a stationary emergency vehicle or tow truck displaying flashing amber warning lights. You can review this and other important California driving regulations on the official California Driver’s Handbook page. Following these laws not only keeps first responders safe but is also a key part of the responsible driving habits taught in driver education.

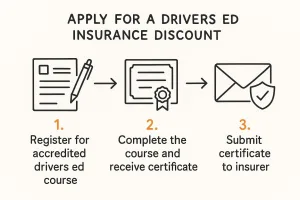

A Simple Guide to Claiming Your Discount

You did it. You finished the driver’s education course, which is a huge accomplishment. But the best part is still to come: turning that hard work into actual savings on your car insurance. Claiming your insurance discount for drivers ed is usually simple, but knowing the exact steps will get that money in your pocket as fast as possible. This quick visual guide breaks down exactly what you need to do next. As you can see, the path from course completion to lower insurance rates is direct. Let’s walk through it.

Getting Your Certificate of Completion

First things first, you need the official proof. After you pass your state-approved course, the driving school will issue your Certificate of Completion. This document is the golden ticket your insurance company needs to see. Most schools send this out automatically. You will likely get it as a digital copy via email, but some might still mail a physical one.

Sending the Proof to Your Insurance Company

Once you have that certificate, it is time to talk to your insurance agent. You have to be proactive. Insurers will not know you completed the course unless you tell them. So, do not just assume the discount will magically appear on your next bill. Forgetting this crucial step can cause you to miss out on months of savings.

Checklist for Claiming Your Insurance Discount

This checklist will guide you through the process, step by step. Following this makes it almost impossible for your request to fall through the cracks.

Step

Action Required

Key Tip

1. Initial Contact

Call or email your insurance agent. Tell them you have completed a state-approved driver education course.

Have your policy number ready to speed things up. Be direct: “I’m calling to apply my driver’s ed discount.”

2. Submit Proof

Send a copy of your Certificate of Completion. Your agent will tell you their preferred method (email, fax, or online portal).

Take a clear photo or scan of your certificate. Make sure your name and the completion date are easily readable.

3. Get Confirmation

Ask the agent to send you a confirmation email or written notice showing the discount has been applied to your policy.

This creates a paper trail. If the discount does not show up later, you have proof of your request.

4. Verify the Savings

Carefully review your next insurance statement. You should see a line item for the discount or a lower overall premium.

Do not just look at the total! Compare it to your previous bill to see the exact amount you’re saving.

By following these simple steps, you are actively managing your policy and making sure you get every dollar of savings you’re entitled to.

What to Do If the Discount Isn’t There

So you sent everything in, but your next insurance statement looks exactly the same. What now? Do not panic. Sometimes it just takes a full billing cycle for the changes to take effect. That said, it never hurts to check. Give your agent a polite call. A quick, friendly follow-up is all it usually takes to get things sorted out.

It’s Not Just About the Discount: The Real Value of Driver’s Ed

Sure, the insurance discount is a great reason to take a driver’s ed course. Who does not want to save money? But honestly, that is just the cherry on top. The real, lasting benefit is becoming a safer, more skilled driver for life. Think of it as an investment in your own safety—and the safety of everyone you share the road with. That peace of mind is something you just cannot put a price tag on.

Becoming a Proactive, Defensive Driver for Life

A top-notch driver’s ed program is not just about memorizing traffic signs. It is about teaching you the art of defensive driving—the ability to see trouble coming and steer clear of it before it ever becomes a real threat. These are practical, real-world skills that build genuine confidence behind the wheel. You will walk away with crucial abilities, including:

Spotting Hazards Early: Learning to scan the road ahead and identify potential problems is a game-changer.

Mastering Evasive Maneuvers: The course gives you the tools and muscle memory to react instinctively and correctly in an emergency.

Navigating Tricky Conditions: You will learn proven strategies for handling sudden downpours or thick fog, situations that can rattle even seasoned drivers.

Good driver’s ed ingrains responsible habits that stick with you. The whole point is to shift your mindset from simply reacting to traffic to proactively managing the space around your vehicle. This dramatically lowers your chances of ever getting into a collision. The U.S. Department of Transportation (USDOT) provides many resources on safe driving practices that reinforce these concepts.

A Smart Investment in Your Safety

At the end of the day, the real win is building a solid foundation of skill and confidence. A good defensive driving course reinforces the simple, life-saving habits that matter most: always wearing your seat belt, managing your speed, and staying focused on the road. It is this comprehensive training that makes insurance companies so willing to offer a discount. They know it works.

Insurers see the data. Drivers who complete a defensive driving course are statistically safer, which is why they often reward them with premium reductions of 5% to 20%. It is a clear sign of their confidence in the long-term value of this kind of training.

When you sign up, you are not just chasing an insurance discount for drivers ed; you are making a conscious decision to become a better, safer driver. That is the most valuable takeaway of all.

Answering Your Top Questions About Driver’s Ed Insurance Discounts

You have decided to take a driver’s ed course to lower your insurance premium—that is a smart move. But it is natural to have questions about how it all works. Let’s walk through some of the most common things people ask.

How long does a driver’s ed discount last?

This is a great question, and the answer is not always the same for everyone. For new teenage drivers, insurance companies often let the discount ride until you turn 25. That is typically the age when rates start to drop naturally anyway, assuming you have kept a clean record. If you are an experienced driver taking a course, the discount is usually valid for about three years. After that, you will likely need to take a refresher course to keep the savings. Your best bet is to call your insurance agent. They can tell you exactly what their terms are.

Do insurance companies accept online driver’s ed courses?

Yes, most do! The convenience of online courses is a huge plus, and many insurers recognize them. However, there is a crucial catch. The course must be state-approved. An insurer will not give you a discount for a random course they have never heard of. It has to be certified by your state’s official licensing authority. Before you enroll, double-check with your insurance provider. Ask them specifically if they accept the online course you are considering for a premium reduction.

What happens to the discount if I get a ticket?

Think of the driver’s ed discount as a reward for being a safe, low-risk driver. If you get a moving violation or cause a collision, you are signaling to the insurance company that the risk has gone up. When your policy comes up for renewal, they will pull your driving record. A new ticket or incident will almost certainly cause them to remove the discount. The course teaches you the skills, but it is your consistent, safe driving that keeps the savings locked in.

Does every insurance company offer this discount?

While it is incredibly common, it is not guaranteed. The vast majority of major auto insurers provide some kind of discount for completing an approved driver education course, but the specifics can vary wildly. The discount amount, rules about online courses, and age restrictions can all change from one company to the next. Never just assume you will get the discount. The single smartest thing you can do is call your insurance company first. Confirm they offer it and ask for their specific requirements before you sign up for any class. Ready to become a safer driver and start saving? Taking a state-approved course is an easy way to learn essential driving skills on your schedule. Enroll in a course today!

Discover what advanced driver education covers, how it differs from basic courses, and how Florida drivers can earn insurance discounts and dismiss points.

Learning disability accommodations explained for school, work, and online courses. Learn eligibility, documentation, and how to request the right supports.

Find the right clases de manejo en espanol in Florida. Compare BDI, IDI, aggressive and mature driver courses, online vs in-person, costs, and certificates.