That sinking feeling when you see flashing lights in your rearview mirror is universal. After the stress of a speeding ticket, the next big question is, how long will this stay on my record?

While every state has its own rules, a typical speeding ticket will stay on your driving record for about three to five years. Think of your driving record as a report card for the road. Insurance companies and law enforcement review it, and a ticket is a mark that can linger for a while.

Understanding Your Driving Record and Speeding Tickets

Your driving record is the official story of you as a driver. In short, it is a complete history that includes your license status, personal details, and any traffic violations or collisions.

When you get a speeding ticket and either pay it or are found guilty, the violation gets logged on your record. At that point, it becomes visible to anyone with authorized access. This visibility often leads to the real financial sting from insurance companies.

Insurers use your driving record to calculate how much of a risk you are. For instance, a speeding ticket suggests you are more likely to be in a crash. As a result, that risk often translates into higher premiums. Keeping your record clean is a major factor in keeping your insurance rates from climbing.

How Long Does a Ticket Actually Stay On Your Record?

The lifespan of a speeding ticket on your driving record depends on where you live. The rules can change a lot from one state to another.

The general rule is three to five years, but it is not a one-size-fits-all answer. For example, a standard speeding ticket in California stays on your record for three years. In contrast, a ticket in a state like Florida could stick around for up to five years. This window of time is what your insurance provider looks at when they decide how much you will pay.

Many people think that paying the fine makes the ticket vanish. In fact, paying the fine is an admission of guilt. Once you pay, the violation is officially on your record. For more information on road safety, you can visit the National Highway Traffic Safety Administration (NHTSA).

The first step to dealing with a ticket is knowing your state’s specific rules. For instance, those in the Sunshine State can see their history with a Florida driving record check.

Key Takeaway: Your driving record isn’t a permanent stain. Violations do eventually fall off, but the hit to your insurance rates can linger for several years even after the points are gone.

Understanding these timelines is crucial because it empowers you to be proactive. For many drivers, the best strategy is to find ways to prevent points from being added to their license in the first place. That’s how you truly protect both your record and your bank account.

Typical Duration of Speeding Tickets on Driving Records by State

To give you a clearer idea of how much rules can differ, here’s a quick look at how long a typical speeding ticket stays on a driving record in various states.

| State | Typical Retention Period |

|---|---|

| California | 3 years |

| New York | 3 years (until the end of the year it occurred) |

| Texas | 3 years |

| Florida | 3-5 years (depending on severity) |

| Pennsylvania | 5 years after suspension/revocation is resolved |

| Virginia | 5-11 years (depending on severity) |

| Nevada | 1 year for demerit points, but visible longer |

As you can see, the “standard” isn’t so standard after all. This is why it’s so important to understand the local laws that apply to you whenever you get a traffic citation.

How the Driver’s License Point System Works

Most states, including Florida, use a point system to track driving violations. It’s a straightforward way for the Department of Motor Vehicles (DMV) to keep an eye on things. When you are convicted of a moving violation, like a speeding ticket, points get added to your driving record.

Think of it like a demerit system. In short, you want to keep your score as low as possible. Every ticket adds points. If you get too many points in a certain time, you will face serious consequences. The biggest consequence is a suspended license, which means you cannot legally drive.

A Closer Look at Florida’s Point System

Let’s look at how this works in Florida. The Florida Highway Safety and Motor Vehicles (FLHSMV) department assigns points based on how serious the violation was.

For speeding, the breakdown is clear:

- 3 Points: This is for going 15 mph or less over the speed limit.

- 4 Points: If you’re caught driving 16 mph or more over the limit, you get 4 points.

- 6 Points: This is the most severe. It is for situations where your speeding leads to a crash.

It’s easy to see how a few tickets can quickly put your license in danger. The state has very specific rules about how many points cause a suspension.

When Do Points Turn Into a Suspension?

In Florida, timing is very important. The FLHSMV looks at how quickly you get points. This is how they find drivers who are repeatedly making bad choices.

They have set timelines. If you hit a certain number of points within one of those windows, your license gets suspended. The rules are clear for everyone. You can learn more about safe driving practices from the Governors Highway Safety Association (GHSA).

Accumulating just 12 points within a 12-month period is enough to trigger an automatic 30-day suspension. This can happen faster than most drivers realize, often with just three or four tickets.

Here are the specific thresholds that every Florida driver needs to know:

- 12 points in 12 months will get you a 30-day suspension.

- 18 points in 18 months leads to a 3-month suspension.

- 24 points in 36 months means you’ll face a 1-year suspension.

Knowing exactly how many points lead to a suspended license is the first step in protecting your driving privileges. It’s a crucial part of being a responsible driver.

State Spotlight: Speed Management Rules in California

Every state has unique roadway laws. California, for example, has very specific rules about speed management that every driver should know. These laws are designed to keep everyone safe on the road.

California’s “Basic Speed Law” is a key rule. It says you must never drive faster than is safe for current conditions. This means even if the speed limit is 65 mph, you might need to drive slower if there is heavy traffic, bad weather, or road construction. You can find the full details in the official California Driver’s Handbook.

Another important rule is the “Move Over” law. In California, if you see a stationary emergency vehicle or tow truck with flashing lights on the side of the road, you must move over to another lane if it is safe to do so. If you cannot move over, you must slow down to a reasonable and prudent speed. Following this law protects police, firefighters, and other emergency workers.

How Speeding Tickets Impact Your Insurance Rates

The initial fine for a speeding ticket is bad enough. However, the real financial pain often comes from your car insurance. Insurance companies are all about managing risk. Therefore, they use your driving record to predict your chances of getting into a crash.

When you have a clean record, you seem like a safe, low-risk driver. As a result, your insurance rates stay affordable. But a speeding ticket changes that entire calculation.

Think of it like a late payment on your credit score. That one mistake can make your insurance premium jump. That higher rate often stays with you for the entire three to five years the ticket remains on your record. Over time, that adds up to much more than the original ticket cost.

The Financial Cost of a Violation

It is pretty simple: the faster you were going, the more you can expect to pay. A ticket for driving 20 mph over the speed limit looks much riskier to an insurer than one for just 10 mph over. Consequently, the penalty from your insurance company will reflect that.

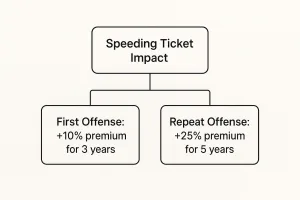

In fact, a single speeding violation can raise your annual premium by 20% to 30%. It all depends on your insurance provider and the ticket details. Suddenly, a small mistake becomes a big, expensive problem that strains your budget for years.

How Insurers View Your Record

Insurance companies look at your whole driving history when deciding your rate.

- First-Time Offenders: If this is your very first ticket, you might get a break. Some insurers even have “ticket forgiveness” programs for a first minor violation.

- Repeat Violations: Getting multiple tickets in a short time is a huge red flag. It tells the insurer you are a high-risk driver, which can lead to big premium increases.

- Severity of the Offense: Not all tickets are the same. For example, speeding in a school zone is taken far more seriously than a minor infraction.

Your driving record is one of the biggest factors that determines what you pay for car insurance. A speeding ticket signals that your risk profile has changed, and they’ll adjust your premium to match.

The good news is that these rate hikes are not forever. Once a ticket ages and drops off your record, your rates should come back down. However, you must keep your record clean from that point on. If you want to be proactive, there are ways you can work to lower your insurance premiums, even with a ticket on your record.

Taking Control: Options for Handling a Ticket

Getting a speeding ticket is frustrating. However, knowing what to do next is the real key.

Fortunately, you have options to protect your driving record and keep your insurance rates from rising. The most effective route for many drivers is to complete a state-approved driver improvement course. It is a proactive step that shows you are serious about safe driving. This can help you prevent bigger problems down the road.

Take a Driver Improvement Course

In many states, you can attend a defensive driving class after getting a ticket. This is often known as a Basic Driver Improvement (BDI) course. Taking this class can be a total game-changer for your record.

When you complete a BDI course, the court may agree to “withhold adjudication.” This means that while you still pay the ticket fine, no points are added to your license. This keeps your record clean, which is a massive win for avoiding insurance hikes. You can see exactly how a course can remove points from your license and what it involves.

Is Traffic School an Option for You?

Not every driver can sign up for a driver improvement course. States have specific rules you must meet.

Here’s a quick checklist for eligibility in Florida:

- You cannot have taken a BDI course in the past 12 months.

- You can only use this option five times in your life.

- The ticket must be for a non-criminal moving violation.

- You cannot hold a Commercial Driver’s License (CDL).

It is critical to confirm your eligibility with the clerk of court in the county where you got the ticket. You must elect to take the course within 30 days of the citation date. If you miss that window, the chance to keep points off your record is gone for good.

Exploring Other Legal Avenues

Beyond a defensive driving class, there are other ways to handle a violation. You might find expungement and record sealing options. These are legal processes that ask a court to clear or hide a violation from public view.

This legal path is typically for more serious offenses and almost always requires an attorney. For a standard speeding ticket, a BDI course is by far the most straightforward and cost-effective solution.

When you get a ticket, you are at a crossroads. You can pay the fine and take the points, or you can take action. Choosing a BDI course is an investment in your driving future. It helps you keep your record clean and your insurance costs under control.

Your Speeding Ticket Questions Answered

If you’ve recently received a ticket, you probably have many questions. Let’s walk through some common questions drivers have about speeding tickets and what comes next.

Do speeding tickets stay on your record forever?

No, speeding tickets do not stay on your record forever. In most states, a minor speeding ticket will remain on your driving record for three to five years. After that period, it should no longer affect your insurance rates or be visible for most background checks.

How can I check my driving record?

You can get a copy of your official driving record from your state’s Department of Motor Vehicles (DMV) or equivalent agency. Most states allow you to request your record online, by mail, or in person at a service center. This will show you any active points and violations.

Will an out-of-state ticket affect my record?

Yes, it most likely will. Nearly all states share traffic violation information through the Driver License Compact (DLC). This agreement means a ticket you get in another state will be reported back to your home state’s DMV and will appear on your record. The U.S. Department of Transportation (USDOT) provides information on interstate travel and regulations.

What happens if I don’t pay a speeding ticket?

Ignoring a speeding ticket will make the situation much worse. The court can issue a warrant for your arrest. In addition, your driver’s license will likely be suspended for failure to pay. Driving with a suspended license is a serious offense that can lead to large fines and even jail time.

How do points affect car insurance rates?

Insurance companies see points on your record as a sign of risky driving. More points usually mean higher insurance premiums. A single speeding ticket can cause your rates to increase by 20-30% for the entire time the ticket is on your record, which can be several years.

Can a defensive driving class remove points?

In many states, yes. Successfully completing a state-approved defensive driving or driver improvement course may prevent points from being added to your license for an eligible ticket. You should always check with the court in the county where you received the ticket to confirm your eligibility.

Ready to protect your driving record and keep your insurance rates from climbing? BDISchool offers a state-approved online Basic Driver Improvement course that can help you avoid points on your license for an eligible ticket.